Could Your Social Media Profile Be Hurting Your Chances of Getting a Mortgage?

Beth Helvey April 18, 2025

Beth Helvey April 18, 2025

A lot of people share a lot about their lives online. The highs. The lows. The wins. The rants. That vacation sunset. The new puppy. The less glamorous stuff too—bad days, broken appliances, job frustrations.

It’s easy to understand why. Social media can be a great place to let off steam, get a little affirmation, and feel like you’re not alone in your stress or your triumph.

But if you’re thinking about buying a home—or you’ve already applied for a mortgage—now might be a good time to pause before you post. Because while social media might feel like your personal space, it’s not as private as you think. And in some cases, it could even affect your ability to get a loan.

Most buyers know the basics when it comes to getting ready for a mortgage. They check their credit score, save up for a down payment, and gather all the necessary documentation like bank statements and tax returns. All good things to have in order.

But here’s one thing that often gets overlooked—your online presence.

According to a recent Realtor.com article, some mortgage lenders are taking borrowers’ digital footprints into account when assessing applications, especially if there are red flags or gaps in documentation.

In particular, LinkedIn is becoming a go-to tool. A borrower’s profile can help confirm things like job titles, dates of employment, business activity, and even geographic location. Some tech companies are reportedly experimenting with web-scraping tools to help lenders analyze online data for risk.

This isn’t a formal or universal part of the underwriting process (yet), and most traditional lenders aren’t scrolling your TikTok at 2 a.m. looking for dance videos and dinner photos. But when there’s something in your file that needs a closer look—like inconsistent employment history or unverifiable income—some lenders are starting to do their own digital sleuthing.

If a loan officer is combing through a borrower’s social media profiles, they’re not doing it out of boredom. They’re looking for context.

Inconsistent job history or employment gaps may prompt a peek at LinkedIn to verify titles, timelines, or whether a business actually exists.

For example, here are a few things that might raise questions:

If what’s online doesn’t match what’s on your application, they may dig deeper.

They may also be trying to get a sense of stability—does this person seem settled in their career and financial life, or are there signs of turmoil? Are they careful about spending, or living a lavish lifestyle?

So while you don’t have to worry about lenders looking through and judging your vacation pics if they’re in line with what they’d expect given your income and assets, those sunset shots could set off alarms if they feel like you might be living beyond your means.

This doesn’t mean you need to erase your digital life. But if you’re planning to apply for a mortgage—or you’re already in the process—it’s smart to do a little online housekeeping.

Here are a few ways to protect your chances:

For small business owners and self-employed buyers, a strong digital presence can actually help your mortgage application.

A well-maintained website, active business social media accounts, and an up-to-date LinkedIn profile can all lend credibility to your business. If your tax documents alone don’t paint a full picture, a lender might find reassurance in knowing that your business is real, active, and viable.

But a word of caution—don’t try to suddenly manufacture an online presence right before applying for a mortgage. A flurry of posts after months of silence can look like you’re trying to build a story, not reflect reality. Your digital footprint should reflect long-term stability, not last-minute PR.

The Takeaway:

Social media probably won’t make or break your mortgage approval. But in today’s lending world, where underwriters are digging deeper and lenders are exploring new ways to assess risk, your online presence could tip the scales.

If your credit, income, and documents are rock solid, you probably won’t be affected. But if your application has a few question marks, don’t let an old tweet or an inconsistent job title on LinkedIn raise more.

Remember that anything you post online could be viewed through a different lens—one that’s focused on financial risk, not likes and comments. Before you apply for a loan, give your online presence the same attention you give your paperwork.

A rare opportunity to own a piece of Sarasota design history—fully updated for today’s lifestyle.

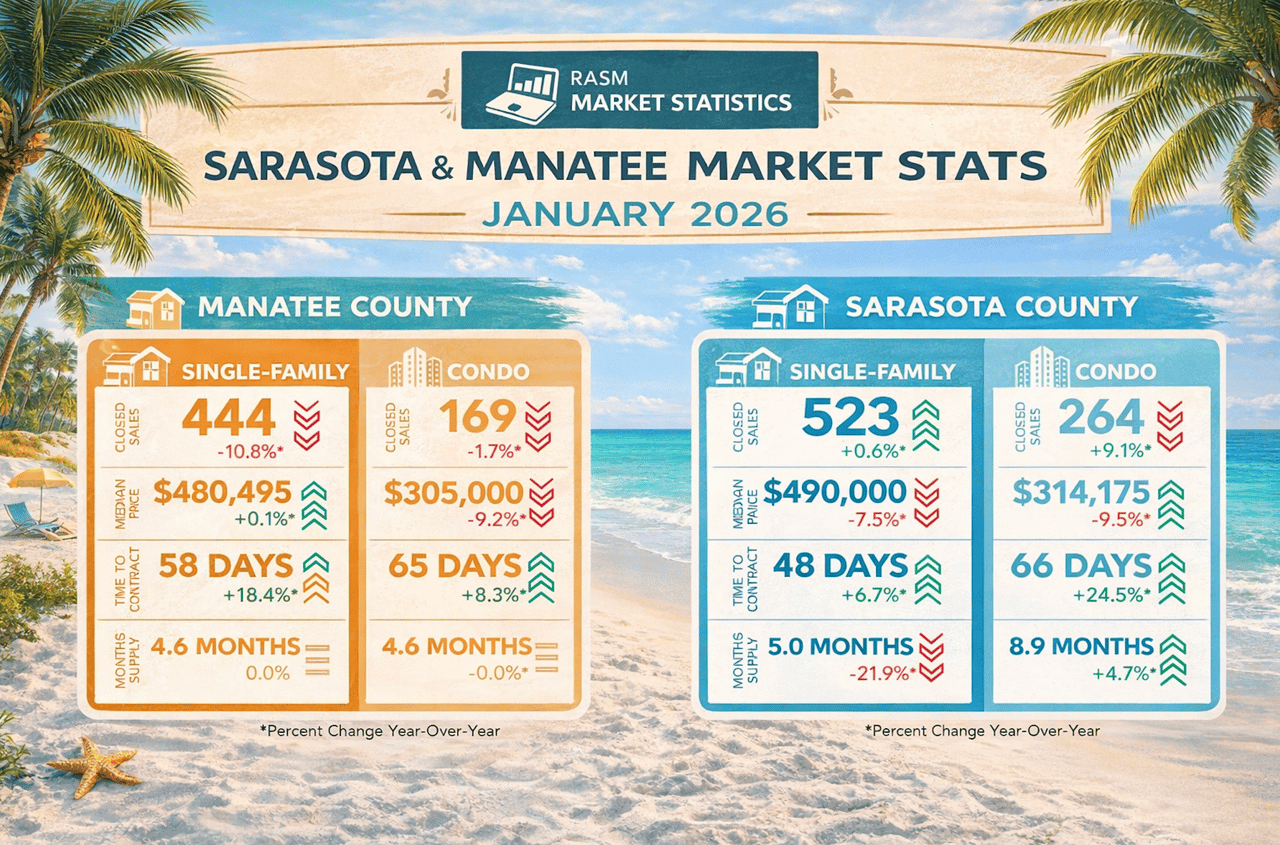

Explore the latest Sarasota real estate market trends for Feb 23 – March 1, 2026. See updates on pending sales, closed transactions, price changes, and buyer activity … Read more

How to Prep for a Mortgage Before You Fall in Love With a House

Freezing = anything that requires a jacket we forgot we owned

Market Report for January 5-11,2025

I’d love to hear from you! Whether you’re buying, selling, or just exploring your options, I'm here to provide answers, insights, and the support you need. Contact me and start planning your next move.