Your Car Payment May Be Costing You More House than You Think

Beth Helvey December 2, 2025

Beth Helvey December 2, 2025

If you’ve ever bought a home before, you’re probably familiar with the advice that agents give their clients: don’t make any big purchases while you’re in the middle of house hunting.

“Big purchases” can mean a lot of things—opening new lines of credit, splurging on furniture, committing to a pricey vacation, or upgrading appliances. And, of course, the one agents mention the most…a new car.

Even with that warning, it’s easy to see how some buyers slip. Life happens. Sometimes it’s a planned purchase, sometimes it’s impulsive, and sometimes it’s just unavoidable. A new car can sneak into the budget without realizing its ripple effects. Yet these decisions can dramatically impact how much home a buyer can afford, or even whether they qualify for a mortgage at all.

Cars aren’t exactly optional for most people. You can’t always time a broken-down engine or a growing family’s need for extra space to line up with your home buying schedule. And some buyers may have purchased a vehicle months before they even began house hunting, not fully aware of the impact it could have on their homebuying power.

But to the degree that it is in your control, understanding the numbers can make a huge difference when planning for a mortgage.

Defining exactly how much a car payment will impact a buyer’s home affordability isn’t something you can do in a vacuum. It depends on income, other debts, interest rates, and a host of personal financial factors. That said, looking at a few different analyses can give a clear sense of just how significant even a moderate auto loan can be.

According to Mortgage Research Network, each additional $100 in monthly car payment can reduce a buyer’s home-buying power by roughly $14,000. For example, a $600 car payment could potentially lower the maximum home price by more than $80,000.

A similar analysis from Refi.com finds that every $100 in car payment reduces mortgage-qualifying potential by about $15,400. At that rate, a $600 monthly payment could shrink a buyer’s mortgage-eligible price by nearly $90,000, depending on other debts and financial circumstances.

And last, but certainly not least… Realtor.com suggested that a $430 car payment could reduce a borrower’s mortgage borrowing power by as much as $100,000 in certain situations.

To put this in context, the average monthly car payment in the U.S. for a new vehicle is around $700, while the average for a used car sits closer to $500. And that’s just one vehicle—many households carry payments on multiple cars. When you start stacking those payments, it quickly becomes clear that the vehicles in your driveway can have a surprisingly large impact on the home that driveway leads to.

Seeing how much even a single car payment can reduce homebuying power makes it all the more obvious how critical it is to think carefully about buying a car not only during the home buying process, but also before you even start house hunting.

For most buyers, it’s not about forgoing a necessary vehicle, but about making choices that preserve as much buying power as possible. That could mean opting for a used car purchased with cash, choosing a lower-cost vehicle, or delaying a second car until after closing.

For others, living in a walkable neighborhood or one with good public transit can reduce the need for multiple vehicles altogether.

Even small adjustments—like refinancing an existing auto loan or paying down debt before applying for a mortgage—can add tens of thousands of dollars to what a buyer could afford.

Every decision around transportation affects the home you can realistically buy. With that perspective, you can make informed choices that balance your daily needs with long-term goals, helping ensure that your car payments don’t shrink your home-buying budget any more than necessary.

It can also be helpful to connect with a local real estate agent and a mortgage professional early on—even if you’re not quite ready to buy. They can provide guidance specific to your situation, run the numbers for your income, debts, and potential car payments, and help you make informed decisions before taking on any new financial obligations.

The Takeaway:

Car payments can significantly reduce how much home a buyer can afford. Even a modest auto loan can translate into tens of thousands of dollars in lost purchasing power—and households with two or more car payments feel that impact even more.

The more you understand how these costs interact with mortgage approval, the more control you have over your homebuying options. Whether that means choosing a lower-cost vehicle, waiting on a purchase, refinancing an existing loan, or exploring walkable, transit-friendly neighborhoods, small decisions can have big ripple effects.

If you’re thinking about buying a home in the near future, looping in a local agent and a mortgage pro early can help you map out the smartest path forward.

Sarasota Real Estate Market Update August 2025: Buyers Stay Active as Back-to-School Season Begins

A rare opportunity to own a piece of Sarasota design history—fully updated for today’s lifestyle.

Explore the latest Sarasota real estate market trends for Feb 23 – March 1, 2026. See updates on pending sales, closed transactions, price changes, and buyer activity … Read more

How to Prep for a Mortgage Before You Fall in Love With a House

Freezing = anything that requires a jacket we forgot we owned

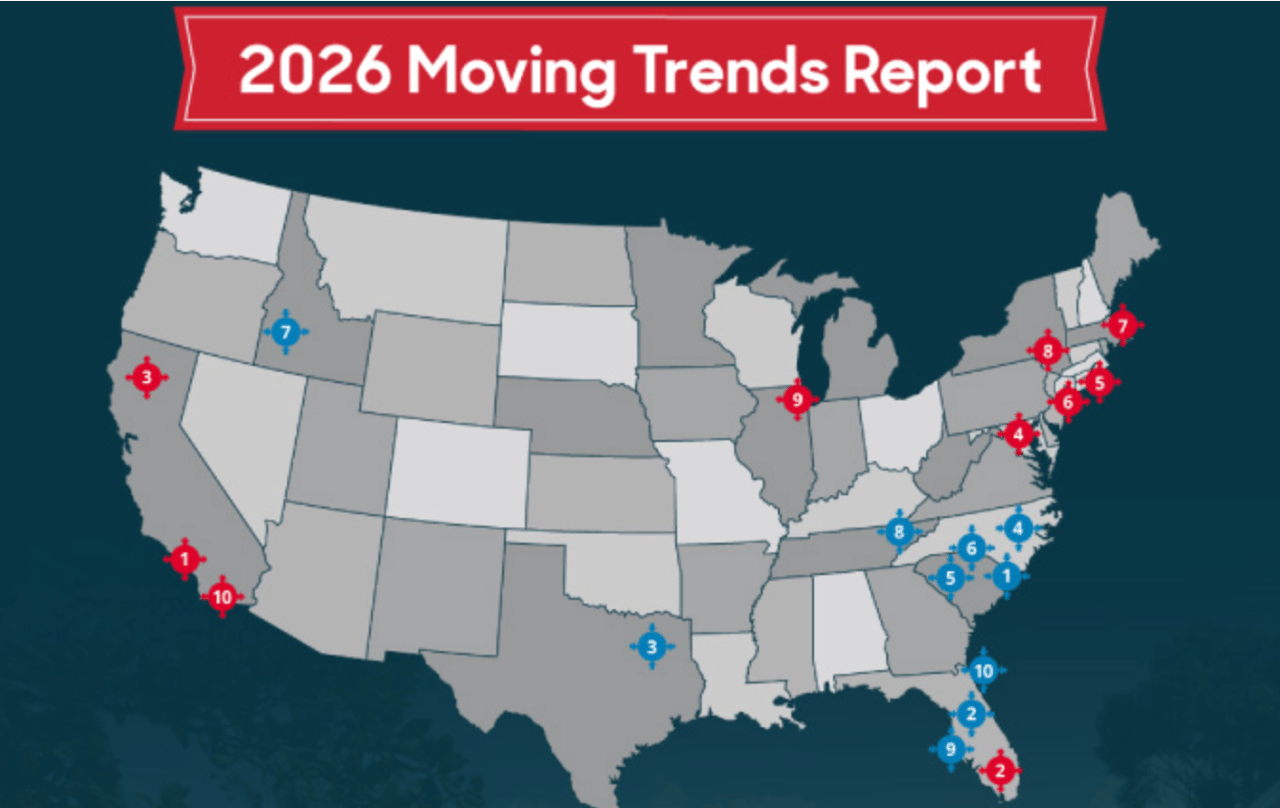

Market Report for January 5-11,2025

I’d love to hear from you! Whether you’re buying, selling, or just exploring your options, I'm here to provide answers, insights, and the support you need. Contact me and start planning your next move.